The Currency That Nobody Spends

Bitcoin has made a lot of people rich, but it just hasn't made them want to spend it.

You’re reading Monday Morning Economist, a free weekly newsletter that explores the economics behind pop culture and current events. You can support the newsletter by sharing it or by becoming a paid subscriber to help it grow:

It’s been seventeen years since a mysterious figure named Satoshi Nakamoto launched Bitcoin in January 2009, born out of a crisis of confidence following the 2008 financial crash. Bitcoin and its peers emerged as an alternative to traditional banking systems that many felt had failed them.

Since then, the predictions have felt relentless. Crypto will replace the dollar. Crypto will make banks obsolete. Crypto will revolutionize how you split dinner, pay your rent, or tip your barista. Every year, a new wave of headlines declares that this is finally the moment mainstream adoption arrives.

Seventeen years later, almost nobody is actually buying anything with it.

The vocabulary is all there: wallets, transactions, exchanges. It looks like money. It’s named like money. So what’s going on? It turns out economists have a very specific definition of what money actually is, and holding crypto up to that definition explains a lot.

And the survey said…

The Federal Reserve recently released the latest edition of the Economic Well-Being of U.S. Households, which it has been publishing annually since 2013. It’s a sweeping look at the financial lives of ordinary Americans, covering topics like how people handle credit, whether they have savings, how they feel about retirement, and whether they could cover an emergency expense. It’s the kind of survey that tells you more about how people actually live than almost any economic report out there.

But one section stood out.

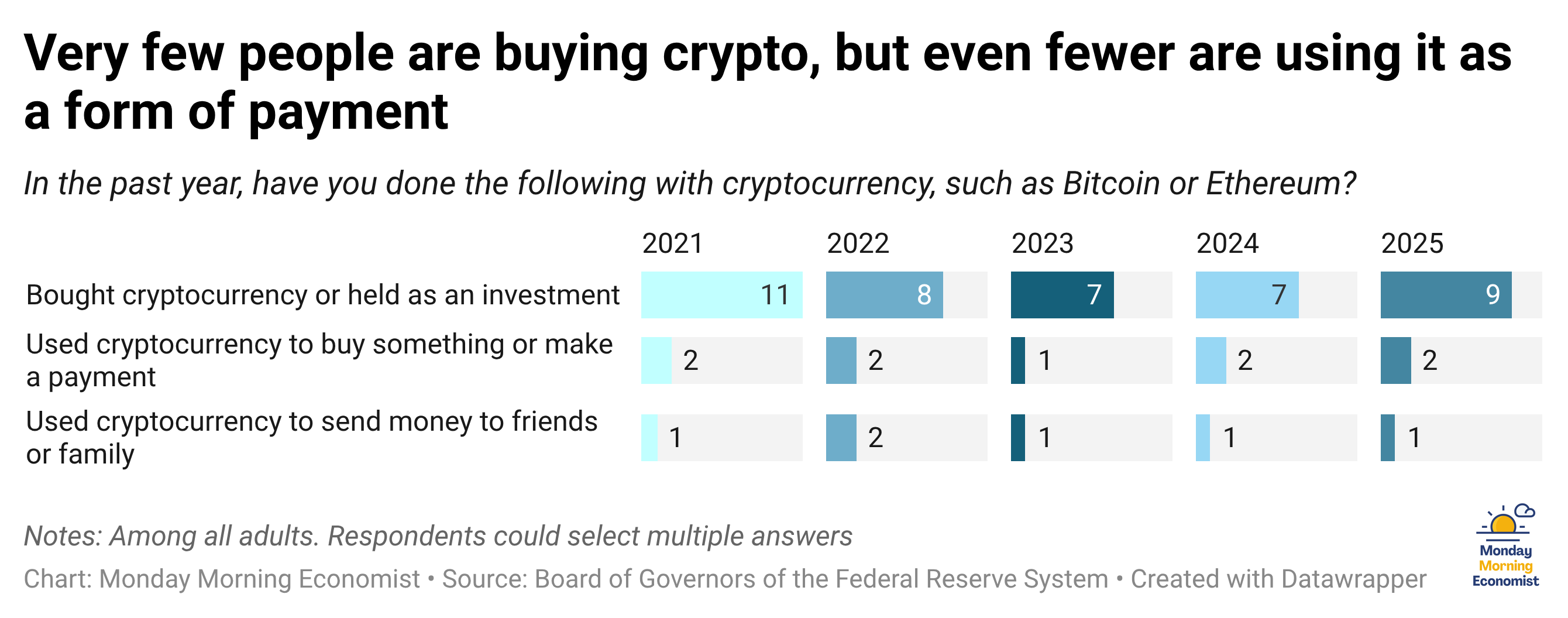

About 10% of adults used crypto in some form last year: buying it, holding it, or transacting with it. That might sound like modest progress, but it’s actually down from 12% in 2021 when the Fed first asked the question.

And even that 10% is misleading. Nearly all of them were simply buying crypto to hold as an investment. Only 2% of adults used it to actually make a purchase or payment.

Which raises a genuinely interesting question: if almost nobody is using it to buy things, is it actually money?

What even is money?

Economists say money has to do three jobs: serve as a medium of exchange, a store of value, and a unit of account. Think of them as three tests. To earn the “money” label, you need to pass all three. Crypto clears one, stumbles through another, and largely skips the third.

Function #1: Medium of Exchange

(Can you actually buy things with it?)

This is money’s most basic job. You work, you get paid, you exchange that payment for food, rent, and concert tickets. The whole point is that it flows easily through the entire economic system. You hand it over, someone accepts it, done.

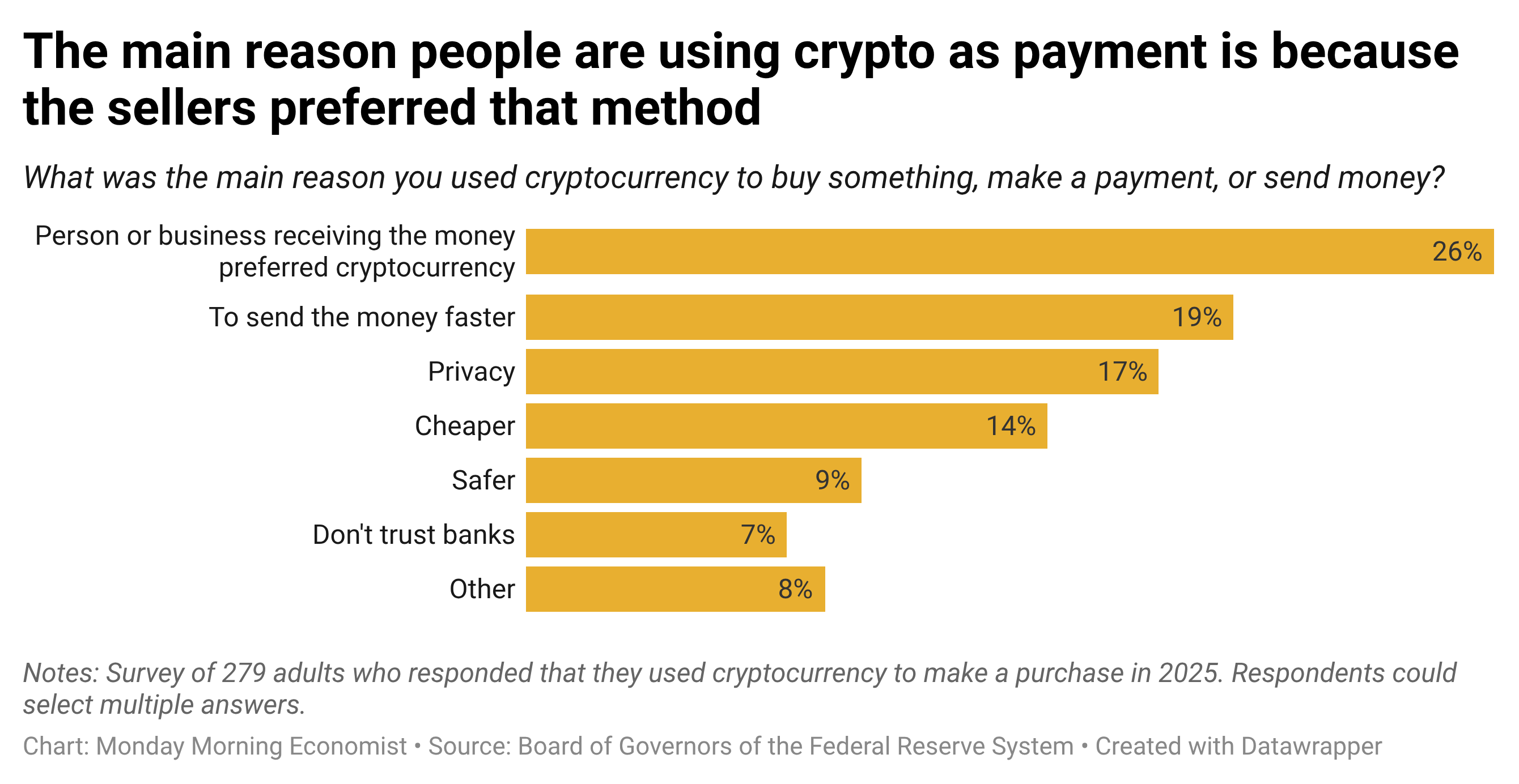

The Fed’s survey gives us a pretty clear verdict on this one. Of the 2% of adults who used crypto for an actual transaction last year, the most common reason was that the person or business on the other end preferred it. Even among the tiny slice of people using crypto as a medium of exchange, most were doing it because someone asked them to. That’s a currency being tolerated, not one gaining traction.

Function #2: Store of Value

(Does it hold purchasing power over time?)

This is where crypto makes its strongest case, but also where things get complicated.

Gold and real estate both hold value. Bitcoin, over the long arc, has increased dramatically. It’s almost certainly why nearly 90% of holders treat it like a stock rather than a spending account. That instinct isn’t wrong. But “store of value” implies some stability, not upward movement.

The dollar quietly loses ground to inflation over decades, but Bitcoin can swing 40% in either direction within a single year. Imagine you’re a freelance designer paid 0.01 Bitcoin for a job in January. That was worth about $950 earlier this year. But wait until April, and that same Bitcoin might be worth only $700. Same work, but far less money. That’s not a store of value.

Function #3: Unit of Account

(Do people price things in Bitcoin?)

This is perhaps the most obvious failure of cryptocurrency over the past decade. A unit of account serves as a measuring stick that allows people to compare prices across different items.

While a growing number of companies are accepting crypto payments, almost nobody prices in Bitcoin. The dollar is still the ruler. Bitcoin has become just a payment option, like Venmo or Apple Pay.

Until something is the thing you instinctively think in, it hasn’t cleared the final bar.

Final Thoughts

There is one argument crypto supporters make that’s worth taking seriously: maybe crypto has failed the three tests because it hasn’t been given a fair opportunity to pass them.

After all, the dollar isn’t money because it’s inherently valuable on its own. It’s money because the U.S. government says it is. We accept dollars not because they’re backed by gold or guaranteed to hold value, but because everyone around us accepts them too. Money, at its core, is a shared fiction that works because we all agree to believe in it.

So what happens when a government decides to extend that belief to Bitcoin?

In 2021, El Salvador tried exactly that. Bitcoin became legal tender. Businesses were legally required to accept it alongside the U.S. dollar. It was the boldest real-world test the “crypto as money” thesis had ever gotten. A whole economy with an actual mandate. If government endorsement is what makes money money, this was the experiment.

Spoiler: it didn’t work. Bitcoin was rarely used by the public, and in 2025, El Salvador quietly rescinded it as legal tender. The Economist called it a failure, one that brought more costs than benefits to the Salvadoran economy.

That’s worth sitting with for at least a few minutes. When a country requires people to treat something as money, and they still reach for something else, that’s not a marketing problem or a government endorsement problem. That’s a functions-of-money problem.

Maybe that changes with a more stable version of crypto that can clear all three bars. Maybe the dollar itself gets replaced by a currency we haven’t named yet.

But perhaps the most interesting question isn’t whether crypto is money, but rather why we’ve been so eager to call it that before it actually was.

If this made you think differently about your wallet, digital or otherwise, share it with someone who uses the word “currency” a little too confidently.

On May 22, 2010, the first commercial purchase occurred when a programmer traded 10,000 BTC for two Papa John’s pizzas [Guinness Book of World Records]

6% of unbanked adults used crypto for payments, compared to 2% of banked adults [U.S. Federal Reserve]

Approximately 2,300 retailers accept cryptocurrency as payment in the United States [Capital One Shopping]

Across all U.S. adults, 63% agree that “cryptocurrencies are not to be trusted” [YouGov]

Data collected in 2024 showed that 8 of 10 Salvadorans did not use Bitcoin, and only 1% of total remittances involved crypto assets [Americas Quarterly]

Two words - pyramid scheme

All you have to do is try to buy and sell bitcoin directly and try to figure out how to even make a purchase and you realize it’s not a thing that any normal person is willing to do. Plus all you ever read is stories about people who lost theirs or forgot the passwords or got kidnapped or hacked because someone heard they had a lot of it. So it’s risky to even admit you own it if you have some. No thanks!

That’s why everyone uses those exchanges, which cause a whole new level of abstraction and complexity. And the Mt Gox commenter tells us what we need to know about that.