What Was the Economy Like in the '90s?

The '90s are having a moment online. Turns out, the economy was having one too.

You’re reading Monday Morning Economist, a free weekly newsletter that explores the economics behind pop culture and current events. Each issue reaches thousands of readers who want to understand the world a little differently. If you enjoy this post, you can support the newsletter by sharing it or by becoming a paid subscriber to help it grow:

If you’ve been on social media lately, you’ve probably seen celebrities and brands posting nostalgic photo slideshows set to the Goo Goo Dolls’ “Iris.” Halle Berry, Drew Barrymore, and Reba McEntire have all been jumping in. And honestly? It tracks.

The ’90s were a cultural moment. Friends and Seinfeld were must-see TV. Kids were rewinding VHS tapes and begging their parents not to cancel Blockbuster night. Everyone had a Walkman and strong opinions about whether frosted tips were a good idea. Even today, Gen Z considers the ’90s as the decade with the best fashion.

I grew up in the ’90s, so naturally I wanted to reminisce too. But I’m an economist. So instead of posting throwback photos, I’ve been thinking about a different kind of throwback: what was the economy like in the ’90s?

Turns out, there’s a lot worth remembering. Cue up The Goo Goo Dolls and let’s get into it.

The Economy at a Glance

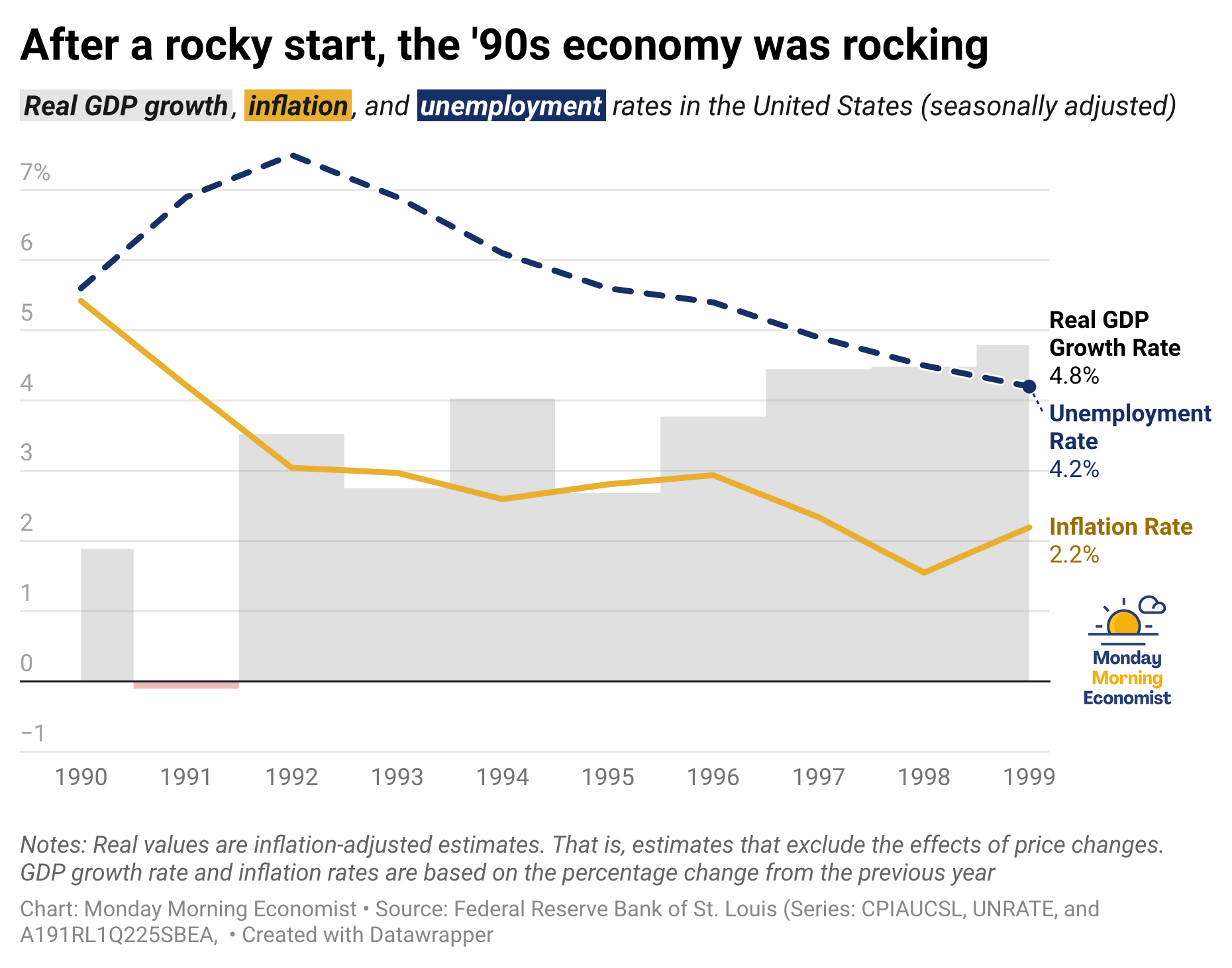

The ‘90s were good. Like, genuinely good. The U.S. created 24 million jobs over the decade, and GDP grew at an average of 3.3% per year. The expansion ran for 120 consecutive months, the longest peacetime run on record. But to understand how it got there, you have to start at the beginning.

The decade opened in rough shape. The banking system was already stressed from the savings and loan crisis of the 1980s, and the 1990 oil price shock following Iraq’s invasion of Kuwait pushed the U.S. into recession. Unemployment climbed to 7.8% by mid-1992. Inflation, meanwhile, was still running above 5%, a hangover from the turbulent ‘70s and ‘80s that the Fed hadn’t fully shaken. Jobs were disappearing, prices were elevated, and the recovery, when it came, was slow. Economists called it a jobless recovery for a reason.

That’s the economy Bill Clinton inherited. His campaign kept a sign on the wall of their war room: “It’s the economy, stupid.” It worked. And once the expansion took hold, it really took hold.

The Fed, led by Alan Greenspan, gradually brought it down to 1.6% by 1998. Low, stable, and largely out of the headlines. That’s usually how you know it’s working. Unemployment followed a similar path, falling steadily through the decade to hit 4% by 2000, a thirty-year low. The U.S. economy was booming. And that boom was about to show up in a very unexpected place.

A Rare Moment of Fiscal Balance

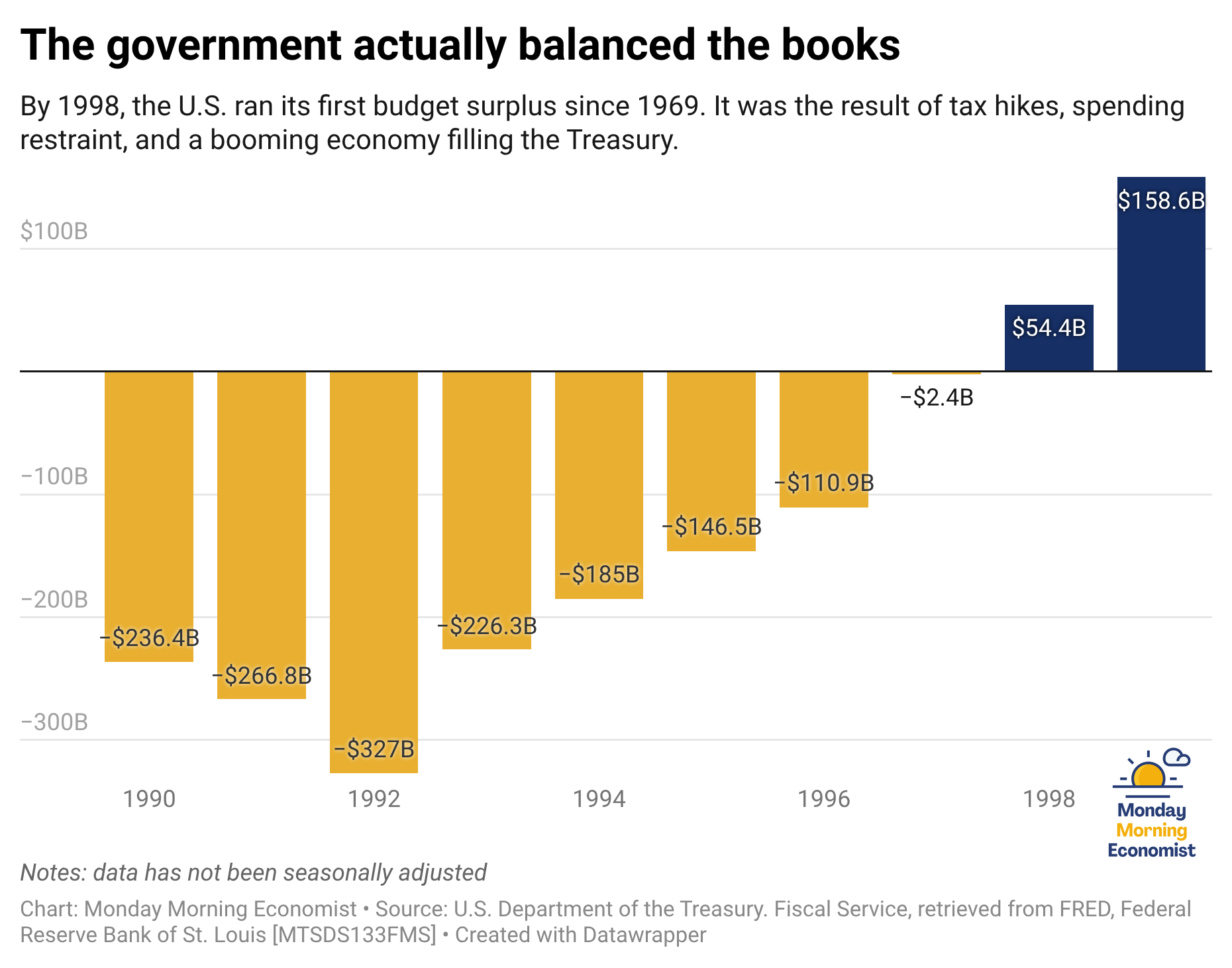

That strong economy led to something that sounds unfathomable today. In 1998, the United States ran a budget surplus for the first time since 1969, and by 2000, it had reached $236 billion.

First, a quick distinction worth making. A deficit is what happens when the government spends more than it takes in during a single year. The debt is the accumulation of all those deficits over time. The U.S. had been running deficits for most of the preceding two decades, and by the early ‘90s, the national debt had grown to roughly $4 trillion. The surplus years didn’t erase that, but they did allow the government to start paying down some it.

So how did the surplus happen? A few things converged. The Clinton administration raised taxes in 1993, and Congress agreed to caps on discretionary spending. It was a politically painful package that passed without a single Republican vote. Then the booming economy went to work. More people employed meant more income tax revenue. More corporate profits meant more corporate taxes. The tech boom added a surge of revenue from capital gains as investors cashed out stock options and equity.

This is a good chance to pause and remember that fiscal outcomes are never just the result of policy choices. Our current annual federal deficits have exceeded $1 trillion for several years running. Politicians from both parties have talked about reducing spending, but the other two ingredients that made the ‘90s surplus possible haven’t materialized.

Free Trade Comes to North America

Now let’s talk about two of the biggest events that reshaped the U.S. economy in the 1990s. The first was NAFTA, first popularized by Ronald Reagan and then negotiated by George H.W. Bush. Clinton signed it into law in December 1993, effectively eliminating most tariffs between the United States, Canada, and Mexico. Significant? Yes. Controversial? Also yes.

The motivation was rooted in the theory of comparative advantage, which is the idea that trade is mutually beneficial when countries specialize in what they produce most efficiently. Tariffs get in the way by raising prices for consumers and shielding domestic producers from competition. Take them away, and trade expands. Everyone wins, at least in theory.

At the aggregate level, the numbers backed it up. Trade between the three countries tripled over the decade. U.S.–Mexico trade alone grew from $81 billion in 1993 to $247 billion by 2000. But the gains weren’t evenly shared, and that tension has never really gone away.

Manufacturing jobs in auto parts, textiles, and other industries migrated south where labor costs were lower, leaving real losses behind in the form of job cuts, stagnant wages, and towns hollowed out by plant closures. NAFTA was eventually replaced by the USMCA in 2020, patching gaps around digital trade, intellectual property, and labor standards that didn’t exist as policy concerns in 1994.

In that sense, NAFTA was a useful first draft, but the underlying debate about who bears the cost of free trade remains unresolved. Trade relations between the three countries are under significant strain today, and whether the framework that took decades to build holds up is one of the more consequential open questions in North American economic policy right now.

The Boom Before the Bubble

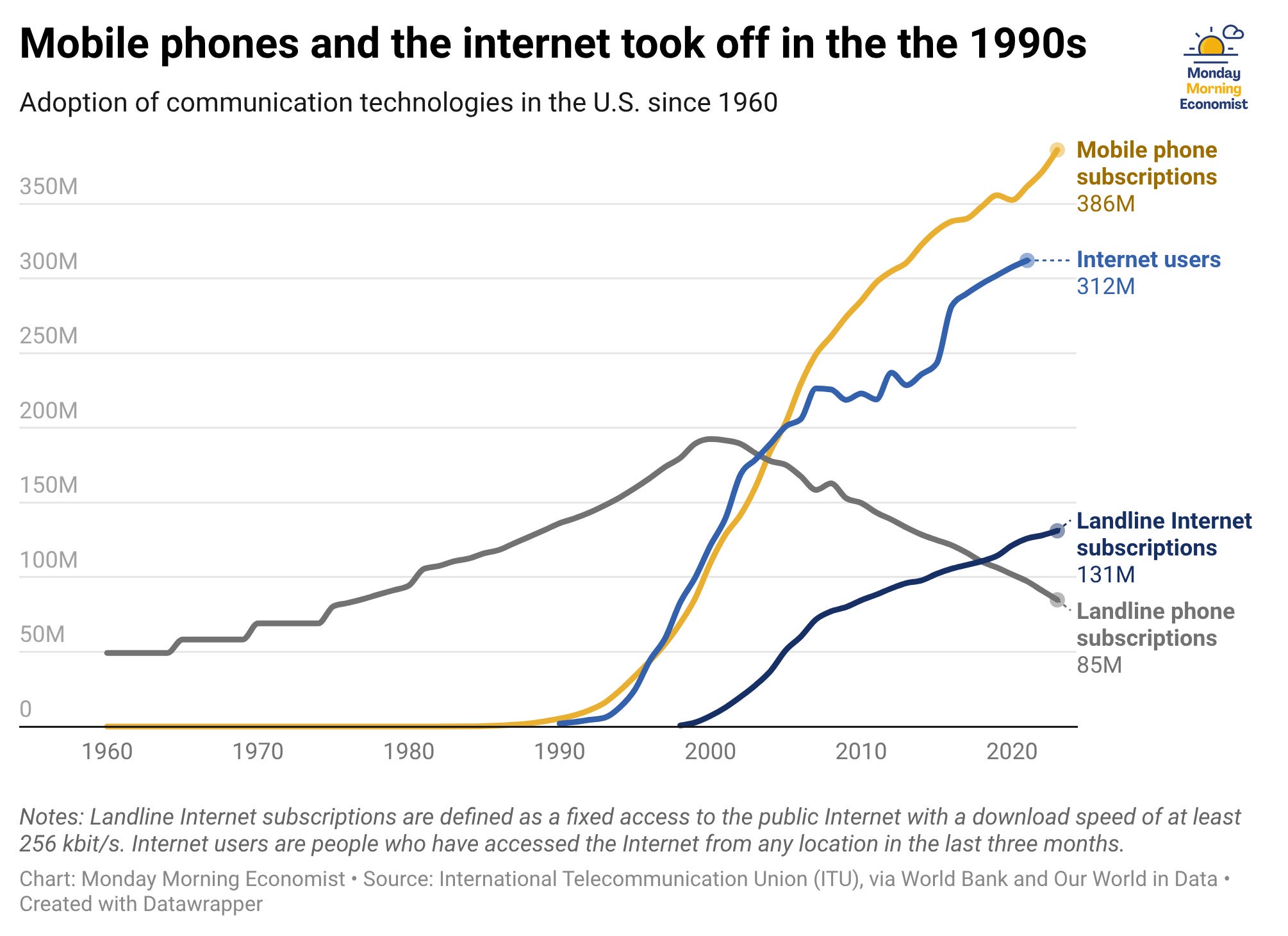

If NAFTA reshaped how goods were made and where, the internet changed how people bought them, accessed information, and interacted with the economy entirely. It’s hard to overstate how different daily life looked by the end of the decade. You could buy a book without going to a store, get news without picking up a newspaper, and send a message to someone across the world for free. And that was just the beginning.

Not everyone saw it coming. In 1998, Nobel Laureate Paul Krugman famously predicted the internet’s economic impact would be no greater than that of the fax machine. It’s one of the more memorable misses in modern economic forecasting.

Investors, on the other hand, saw it coming and easily got carried away. The Nasdaq Composite stood at around 415 in 1990 and hit 4,696 by February 2000, a gain of more than 1,000% in a decade. Companies with no revenue, no profits, and sometimes no clear business model were valued in the billions. The rule of thumb became: if it ends in .com, fund it.

The signs of an asset bubble were hard to miss by the end of the decade. Prices weren’t rising because of underlying value, but rather because buyers expected to sell to someone else at a higher price down the road. When new buyers stopped coming in, the market collapsed fast. The Nasdaq lost 78% of its value over the following two years.

Thankfully, the bubble didn’t erase the underlying technology. Pets.com failed, but Amazon survived and Google launched. By the end of 2000, there were 416 million internet users worldwide, up from 2 million a decade earlier. The business models caught up eventually.

Final Thoughts

The ’90s weren’t perfect. NAFTA had real winners and real losers, and the dot-com bubble wiped out a generation of savings. But the decade also showed what a sustained expansion looks like when the fundamentals line up: low inflation, falling unemployment, rising wages, and (briefly) a balanced budget.

We can even see some of those fundamentals happening in our own economy today. Unemployment is around 4%. Inflation has come back down to the 2–3% range after its post-pandemic spike. GDP growth is more modest, closer to 2%. Some analysts are already asking whether the AI investment boom rhymes a little too closely with the dot-com era.

Of course, the big difference is our federal deficit and national debt. The U.S. had room to maneuver in the ’90s. Today, our national debt is more than the size of the economy, which doesn’t give a whole lot of room to make decisions. The ’90s were a window to what’s possible, but whether we get another one like it is an open question. Overall, not a bad decade to look back on. Even without the Goo Goo Dolls.

Think I missed a bigger economic story? Leave a comment and make the case.

If you know someone who loves the ‘90s or wants to understand the economy a little better, send this their way. I think they’ll appreciate the trip back in time.

65% of Gen Z and 61% of Millennials say the ’90s were fashionable, more than any other decade [YouGov]

Between 1980 and 1994, 1,617 commercial banks failed (9.14% of all banks) with total assets of $206 billion [FDIC]

The federal deficit clocked in at $1.78 trillion in 2025 [U.S. Treasury]

In 2025, the U.S. traded goods worth a combined $872 bilion with Mexico and $719 billion with Canada [U.S. Census Bureau]

5.02 billion people around the world used the internet on a regular basis in 2021 [Our World in Data]

I miss the 90s. I started my academic career in the late 90s before the internet bubble burst. I remember taking Econ classes and the talking point was that the Fed has gotten so good at what they do, we will never see a recession again.

This article really helped me understand why the 1990s economy stands out so much. I didn’t realize how the mix of steady growth, low inflation, and rising productivity made the decade feel unusually stable. The explanations about globalization, NAFTA, and early tech growth also made it clearer how the foundations of today’s economy were being built back then.

One thing I would’ve liked to see a bit more of is how these trends affected everyday people across different income levels. The big-picture view was really helpful, but a little more detail on how households experienced these changes would have made the analysis even stronger.