Why Are Americans Suddenly Saving Again?

An economist’s honest (and annoying) answer would be: “It depends.”

You’re reading Monday Morning Economist, a free weekly newsletter that explores the economics behind pop culture and current events. Each issue reaches thousands of readers who want to understand the world in a slightly different way. If you enjoy this post, you can support the newsletter by sharing it or by becoming a paid subscriber to help it grow:

Your social media feed might look a little different lately. Instead of a lot of vacation photos or shopping hauls, you may have noticed an uptick in the number of people posting about not spending this summer.

“No Buy July” is the latest trend making the rounds. It’s an online challenge where people commit to cutting back on everything but essentials for the month. They’re skipping takeout, pausing subscriptions, and swearing off impulse purchases.

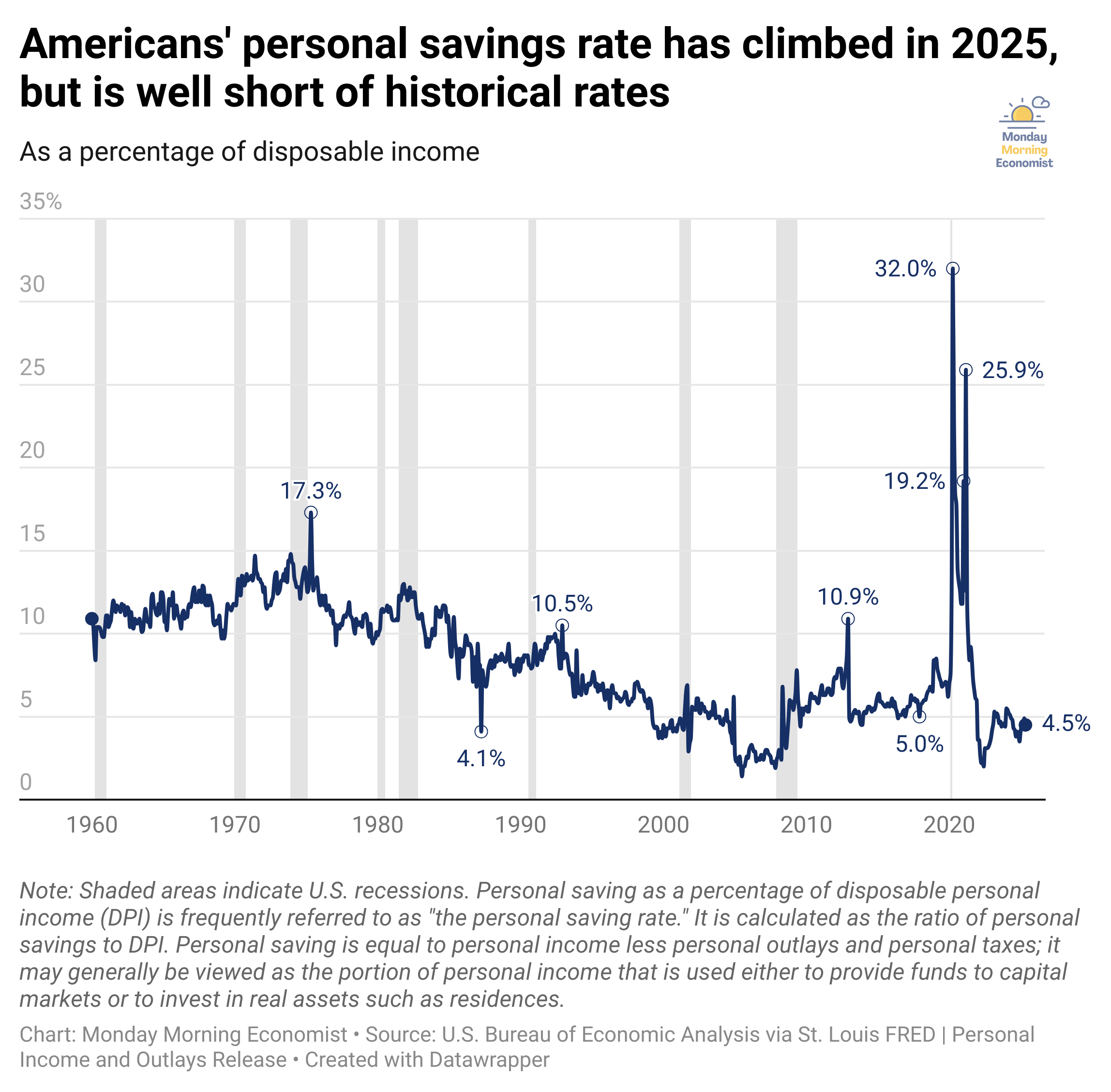

But it’s not just a quirky internet challenge. There has been a shift this year that economists are watching closely: Americans are slowly starting to save more. The share of disposable income people are setting aside has climbed from 3.5% in December to 4.5% in May. That might not sound like much of a change, but even small changes can reveal how people feel about the economy.

But is this rise in savings a sign of financial confidence? Or something more cautious? Let’s take a closer look together.

The Optimistic Take: Higher Earnings, Better Habits

There’s one straightforward explanation for the increase in savings: people finally have some breathing room after more than two years of unusually high inflation rates. After all, our national savings rate is still below pre-pandemic levels.

Prices are still elevated, but the rate of price increases has slowed way down. Over the past few years, real wages have increased over the past few years, with the fastest growth coming from among historically disadvantaged groups. As long as incomes increase faster than prices, households are left with more money at the end of the month. If people have gotten accustomed to trimming their expenses during the recent bout of high inflation, they may have just kept those habits in place.

If this is the underlying cause of the increased savings rate, it would signal that people aren’t nervous about the economy. It means they’re being intentional about their savings.

That intentionality has started to show publicly, too. Hanna Horvath is a Certified Financial Planner, financial editor, and expert in the psychology of money, and has been tracking the rise of “saving culture.” On platforms like TikTok and Instagram, she’s seen a shift from financial shame to financial identity.

Budgeting used to be a private affair, maybe with a spreadsheet you downloaded from the internet. But now it’s getting more public, social, and in some cases, even aspirational. If you’re interested in how our brains shape our financial behavior, Hanna’s videos are worth checking out. She’s on TikTok and Instagram and brings a grounded, psychological perspective to why we spend, save, and sometimes self-sabotage.

The Pessimistic Take: Fear is Driving the Slowdown

Of course, not all saving is a sign of stability. Sometimes people stop spending because they’re worried about the future. It’s what Business Insider has recently dubbed the “Scared Stiff Economy.”

Sure, inflation has cooled from its peak, but that just means prices are increasing more slowly. It doesn’t mean prices have decreased. Groceries, rent, and household bills still feel expensive to a lot of people, and now there's a new concern that’s causing anxiety and confusion: tariffs.

Over the past few months, talk of trade wars has heated up. With constantly shifting tariff policies, consumers may be bracing for another wave of price hikes. That kind of uncertainty can lead people to pull back in the short term. That’s not just on big-ticket items, but on everyday spending too.

And there’s data to back that up. According to the University of Michigan’s consumer sentiment survey, confidence has fallen sharply from 74.0 in December 2024 to 60.7 in June 2025. That’s not just a one-off dip. It’s a sign that households are feeling anxious about the direction of the economy. The Conference Board found similar concerns in their survey of consumer sentiment:

But why does this even matter? Consumer spending drives about two-thirds of U.S. GDP. When people start holding on to their paycheck instead of circulating it through the economy, that can trigger a broader slowdown felt by even more people. Businesses sell less, invest less, and eventually, may hire less.

Economists have a term for this shift in mood: animal spirits. It’s the idea that people’s emotions (e.g., optimism, fear, anxiety) can drive economic outcomes, even if the underlying fundamentals of the economy haven’t changed. If enough people start acting as if a recession is coming, that very behavior can help bring one about.

A lot of people look at the increase in savings rate as a sign that the economy is getting healthier, but it could also be a warning sign. If people are saving more because they’re afraid, that doesn’t point to financial strength. It points to uncertainty and a potential pullback that could ripple through the broader economy.

Final Thoughts

You may be curious about how you and your family can prepare for the uncertainty ahead. I’ll be honest, I can’t answer that for you.

Every household’s financial situation is different, shaped by things like income, debt, family structure, geography, and values. What feels like a safe cushion to one person might feel like a crisis plan to another. That’s why I asked Hanna to join me on this piece. She specializes in how we think and feel about money. I can focus on the big picture around GDP, savings rates, and inflation trends. People like Hanna can help translate those behaviors into real choices, grounded in your everyday life.

At the end of the day, most people aren’t tracking the nation’s savings rate month to month. What they are tracking, consciously or not, is whether the economy feels like it’s headed in the right direction. Whether their job feels stable. Whether groceries feel affordable. Whether the future feels manageable.

And right now, people feel a lot of anxiety.

It’s making the increased savings rate hard to read. But as with most things in economics, a single number doesn’t tell the whole story. The context and “the why” behind the behavior matter more.

If today’s post helped you see the economy a little more clearly, consider subscribing. Each week, I break down the headlines, connect the dots, and show how economics shows up in places you might not expect. No spam. No complicated jargon. Just stories that make you say, “Wait... that’s economics?”

Americans held a collective of $1.013 trillion in personal savings as of May 2025 [Bureau of Economic Analysis via FRED]

The typical American has $8,000 in the bank [The Motley Fool]

Nearly a quarter of employed Americans (23%) aren’t sure how much they’re saving each month, and 10% aren’t regularly saving anything [NerdWallet]

There are more than 107,000 people subscribed to the subreddit r/budget [reddit]

Near the end of 2024, 73% of adults reported “doing okay” financially (39%) or “living comfortably” (34%) [Board of Governors of the Federal Reserve System]

| A guest post by

|

Great post. Increased market uncertainty has led me to increase my savings rate. But also, the resilience of the stock market has been surprising and hard to stay away from

Great article. I too have increased my savings. Mainly because i am forgoing items i use to occasionally buy but are increasing with some of the tariff shocks. I am also finding work arounds for planned electronics purchases i had. For it is out of pessimistic caution for a economy that has some red flags flashing. Granted I am fortunate to work in a field where there is a shortage and i work for a company that historically speaking has been recession resistant, but i do not take anything for granted. Good Job! I really enjoyed todays content.