How Netflix Ruled as a Natural Monopoly of Home Entertainment by Mail

Our story starts in the late 1990s, when VHS tapes were still a thing, and dial-up internet connections were the norm. A little startup dared to challenge the giants of the movie rental business.

Thank you for reading Monday Morning Economist! This is a free weekly newsletter that explores the economics behind pop culture and current events. This newsletter lands in the inbox of thousands of subscribers every week! You can support this newsletter by sharing this free post or becoming a paid supporter:

In the late 1990s and early 2000s, Blockbuster Video was the undisputed king of the movie rental business. With thousands of brick-and-mortar stores scattered across the United States, Blockbuster provided families with access to a vast catalog of films. But then, a disruptive force emerged in the form of Netflix, a company that would eventually redefine how we consume movies.

Founded in 1997 by Reed Hastings and Marc Randolph, Netflix began as a humble DVD rental-by-mail service. The concept was simple but groundbreaking – order movies online and have them delivered to your mailbox. No more late fees, no more trips to the rental store. Just queue up your favorite movies, and they would arrive like clockwork. Renting DVDs through the mail would become so popular that Netflix was once considered the U.S. Postal Service's fifth largest customer.

But how did Netflix manage to grow so quickly to become the dominant player in the DVD rental market? You’ve likely heard about the concept of creative destruction, where entrepreneurs challenge established firms, but why didn't Netflix face more serious competition at the time? Blockbuster would eventually try to offer the same mail delivery service, but it was too late. Netflix’s natural monopoly on rental-by-mail had already been established.

The Characteristics of a Natural Monopoly

A natural monopoly exists when it's most efficient for a single provider to serve an entire market due to certain economic factors. When Netflix was launched, it wasn’t immediately clear that they would become as dominant as they would. Employees hand-stuffed 137 envelopes on launch day in April of 1998. As Netflix grew to millions of subscribers, it quickly became clear that this model wasn’t sustainable. Netflix’s DVD director of engineering Paul Johnson noted:

(Netflix) was growing really, really fast. They had to find a way to automate things because they weren’t going to be able to keep up with the growth.

That investment was expensive, but it turned out that the market had the right mix of all the characteristics it takes to be dominated by a single firm. Let's break down the characteristics that eventually helped Netflix's rise to dominance in DVD rentals.

High Fixed Costs, Low Marginal Costs

Netflix had to invest heavily in building its infrastructure – distribution centers across the country, a sophisticated website, and efficient logistics networks. Those costs were pretty high. At its peak, Netflix was operating more than 50 distribution hubs around the United States. For brick-and-mortar companies, it was likely prohibitive to add the automated equipment Netflix was using:

As Netflix grew and attracted more subscribers, they could distribute those high fixed costs more efficiently. The more DVDs the company could rent out, the lower the average cost of processing each disc. Once they got the average cost down to a profitable level, the additional (marginal) cost of servicing another customer became relatively small. High fixed costs and low marginal costs are a hallmark of natural monopolies. With their investment in automation, Netflix was able to process 1.2 million DVDs each week using a machine that could inspect, clear, and pack 3,500 DVDs per hour.

Economies of Scale

Netflix's ability to scale rapidly as more subscribers joined the service was key to its success. Economies of scale is a concept that focuses on the cost-efficiency of growing a business. It exists whenever a firm lowers its average cost of production when increasing output. The fixed costs that Netflix incurs to operate its processing facilities remain constant regardless of the number of DVDs shipped out.

With a growing subscriber base, they could distribute those high fixed costs more efficiently. So, the more DVDs Netflix rented out, the lower the average cost became for each rental. This enabled the company to offer competitive pricing, attract even more subscribers, and ultimately dominate the DVD rental market.

Large Market Demand

Netflix catered to a vast and diverse market of movie enthusiasts across the United States. It didn’t just offer the latest movies! The demand for movie rentals was a significant and widespread need at the time, which fueled Blockbuster’s growth. Netflix tapped into the desires of movie enthusiasts from all walks of life by offering a wide catalog of options and removing some of the pain points associated with visiting a physical store with a relatively limited selection.

The demand for movie rentals was substantial, and Netflix was perfectly positioned to serve this broad customer base efficiently. Netflix needed a large subscription base to distribute those high fixed costs we mentioned earlier. The significance of a large market cannot be overstated here. Without it, achieving those low average costs would be a challenge.

So, you might be wondering, why didn't other companies jump in and compete with Netflix in the DVD rental-by-mail business? The high fixed costs associated with establishing a DVD rental infrastructure were a significant barrier for potential competitors. Entering a market where Netflix had already secured a substantial portion of the customer base would mean having to share the market, making it less appealing from a business standpoint.

A new competitor would have only been able to grab a small share of the customer pool and then would have been unable to spread their fixed costs across a large base of customers. The new competitor would have had much higher average costs for each movie, which would have made it difficult to earn a profit. Netflix's dominance was solidified because it could distribute its fixed costs across a substantial number of customers, effectively discouraging competition, much like a natural monopoly.

The Transition to Streaming and Beyond

Our story doesn’t end there. Netflix recognized early on that the future of entertainment lay in digital streaming, and that's where they set their sights. It’s essentially another wave of creative destruction in which streaming technology promises instant access without the need for physical discs or postage.

Over the past few years, the streaming wars have become fierce. Netflix has faced growing competition from other streaming services, despite the industry sharing many of the same characteristics that would enable a natural monopoly to thrive. Except for Netflix, streaming services have been losing billions of dollars. It highlights the importance of the last characteristic of a natural monopoly: large market demand.

Acquiring licensing rights for content, producing original programming, and maintaining streaming sites all require large upfront fixed costs. As more subscribers join the site, those fixed costs can be spread across the customer base. Since physical DVDs aren’t being sent out, the marginal cost of another customer is close to zero. The issue? The other streaming companies haven’t been able to acquire enough subscribers to achieve the minimum efficient scale of production necessary to be profitable. Netflix has a large customer base that it established during its DVD-by-mail dominance, which has enabled it to be the only profitable streaming service at the moment.

In 1998, the average video store had between 1,500 and 2,500 titles [The New York Times]

Beetlejuice was the first movie ordered by a customer [Entrepreneur]

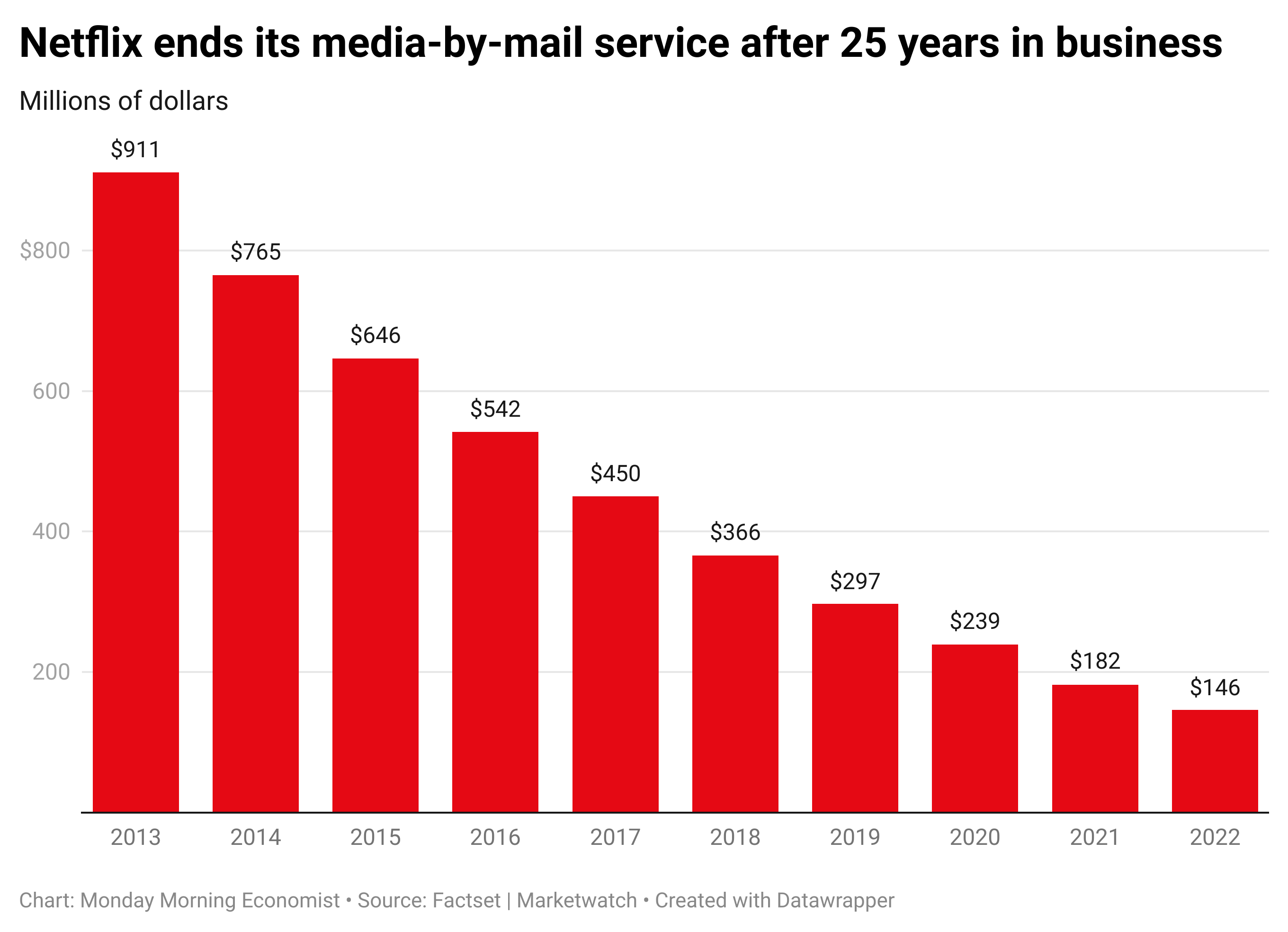

Between 2012 and 2019, when Netflix stopped breaking out revenue for the segment, DVDs generated more than $2.6 billion in profits [The Verge]

Netflix has an estimated global subscriber base of over 238 million accounts [The New York Times]

At its peak in 2011, the company’s DVD-by-mail service (which was only available in the U.S.) hit 20 million customers [Variety]