Buy Now, Pay (More) Later

What could go wrong with four easy payments and 0% interest? A lot.

Back-to-school shopping can get expensive quickly and recent inflationary pressure hasn’t helped. The second half of the summer is a large enough shopping event around the United States that the National Retail Federation ranks it among its top spending events along with the winter holidays. Depending on whether students are heading to school or to college, households were expected to spend between $860 and $1,200 this summer. Many families may be tempted to take advantage of the growing financing trend known as “buy now, pay later,” but understanding behavioral economics can help us see why they may be paying more than they expected.

This financing offer isn’t exclusive to back-to-school shopping, nor is it exclusively an online payment option. I remember taking advantage of buy now, pay later financing when I needed to have my wisdom teeth removed while I was a graduate student. I also used it a couple of years ago when I had air conditioners installed in my home. I’m fairly confident I used it once to pay for new tires as well.

For back-to-college shoppers, they may be in the market for a new laptop; electronics are the largest spending category for that group. In need of a new Macbook? You could pay $1,000 today or pay $83.25 per month for the next 12 months. As long as you don’t miss any payments, you won’t pay any interest and will actually “smooth” your expenses over the next 12 months instead of incurring that cost all at once. This may look like a better deal than charging it to your credit card, which likely has a much higher interest rate.

Consumption smoothing is a situation in which people adjust their spending (and saving) behavior in such a way that they maintain a consistent level of spending over their lifetime. When incomes are higher than expected, people will save more. When incomes are less than expected, people dip into their savings (or use credit) to keep up with their expenses. While great in theory, it relies on a number of constraints that generally make it difficult for a lot of people to implement. An obvious one is people’s access to financial capital.

The buy now, pay later financing option makes it easier for people with limited access to credit to spread their expenses across the year. One common example of the need for such a service comes from the Federal Reserve’s Survey of Household Economics and Decisionmaking. Participants were asked how they would pay for an unexpected $400 expense, such as a car repair or a modest medical bill. In the 2021 survey, 68% of adults said they would have covered the expense exclusively using cash, savings, or a credit card paid off at the next statement. Nearly 1/3rd of adults would need to borrow money, sell something to cover the expense, or just not pay the bill at all:

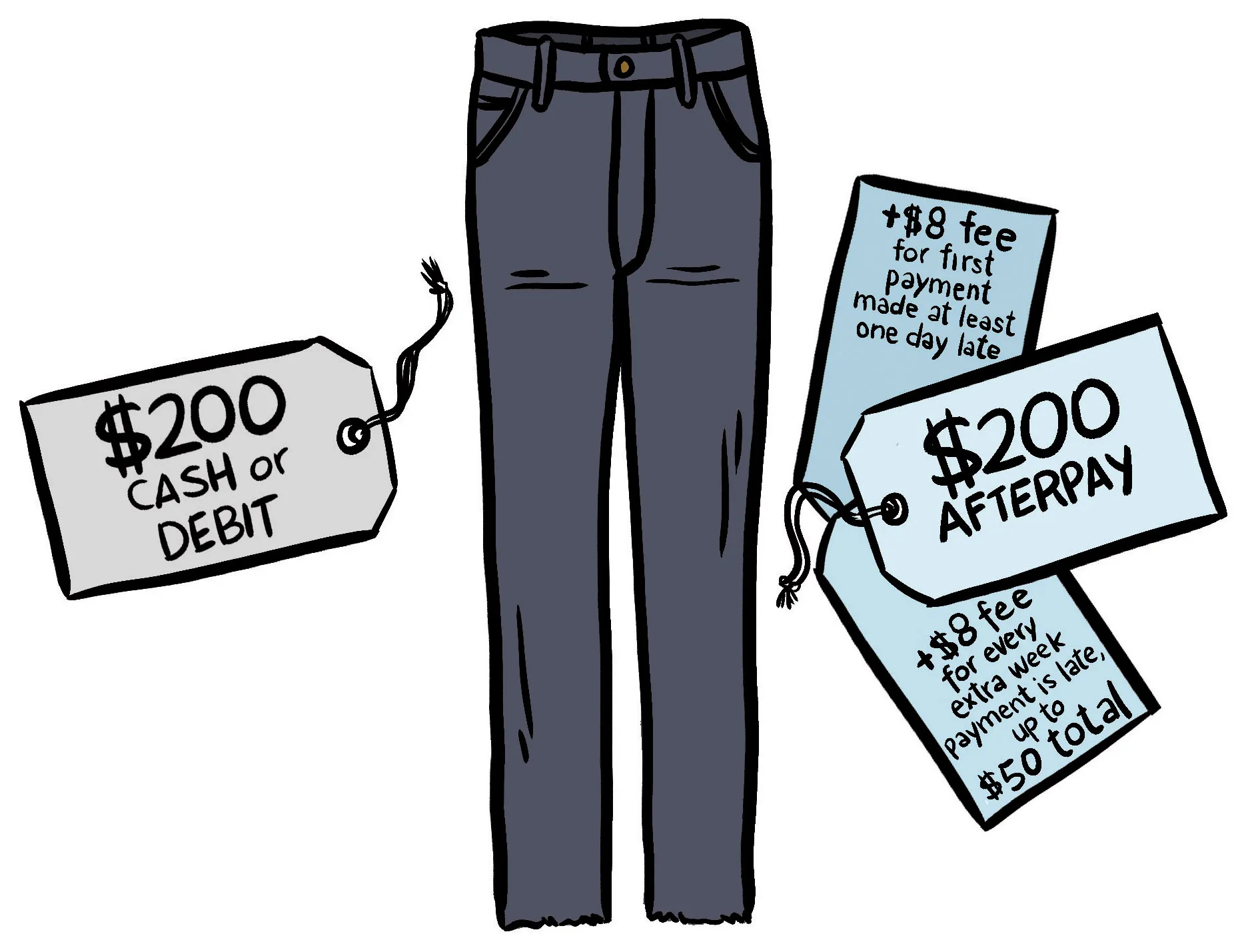

If a $400 expense would be difficult to pay at one time, BNPL financing allows those consumers to spread out the expense over multiple months instead. In theory, it would help people better handle unexpected expenses or infrequent large purchases. The buy now, pay later financing option, however, often results in users spending more money than if they paid for the item at the start. Understanding two key concepts from behavioral economics can help explain why.

The first problem is that people who opt for this financing arrangement tend to spend more money than they would normally. This form of mental accounting tricks people into believing that they are saving money when they’re really spending more money. Spending $100 on the spot may be a lot of money for some people, but breaking a $200 payment into 4 payments of $50 per month seems responsible. It’s easier to put more stuff in the cart when you don’t have to pay as much today for it. In our Macbook example, why just get a laptop when you can also add on some Airpods? The monthly cost would only increase by about $10-$15 per month.

The second issue is that people often have inconsistent time preferences. Jerry Seinfeld articulated the phenomenon as part of his “morning guy” bit on Seinfeld and in his more recent Netflix special. Here’s a summary of one application of inconsistent time preferences that Seinfeld provided for Sirius XM. It focuses on operating at night, but it’s similar to our financing conundrum:

The same concept that tricks the nighttime version of you into behaving differently than the morning version of you also impacts your decisions over longer periods of time as well. When the option to spread payments across the year comes up at the checkout, it seems fiscally responsible since you’re taking advantage of no-interest payments.

The fiscally responsible version of you can’t imagine missing a payment. In a sense, you are practicing financial arbitrage: borrow money from the short-term lender at zero percent interest and take the “savings” to pay down credit card debt or hold money in an interest-bearing account. On the checkout page, it seems like an obvious move. The issue? Buy now, pay later users regularly miss payments.

Missing payments can be incredibly costly since it often means that users will owe back interest on all the previous months and may also have to pay additional fees. Sometimes we miss a payment because we don’t have the income we expected to have, but other times it’s just a matter of forgetting a payment.

Our future selves aren’t the same person we were when we opted for the financing arrangement. It’s easy to think we’ll never miss a payment, but it’s really easy to forget if you aren’t using online banking or if you’re asked to may payments every two weeks instead of monthly.

The biggest concern with these financing programs is who finds them attractive financing options:

Users tend to have lower median household income compared to the general credit population and 1/3 the level of deposits and investable assets.

Applicants have nearly 50% lower bank card limits and their utilization rates are twice as high as the general credit population.

Applicants are 4 times more likely to be subprime than the general population.

So while this financing option provides a meaningful option for households who may not have access to traditional credit options, the repercussions of missing a payment are hitting a group of people who really can’t afford to make a mistake and pay more.

We want people to be able to purchase things when they want to purchase them, and credit is an incredibly important component of our economy. Nearly 7 million people in the US, however, don’t have access to a bank account and nearly 1 in 10 Americans don’t have any credit history with the three nationwide credit reporting companies. We don’t want people to be harmed because of debts they can’t get out of or be taken advantage of by lenders with confusing terms. The Consumer Financial Protection Bureau, unfortunately, has been slow to respond but plans to issue a broader report in the coming months.

66% of adults believe its financially risky to use Buy Now, Pay Later services [C+R Research]

One recent survey found that 42% of Americans who have taken out a BNPL loan have made at least one late payment on it [LendingTree]

Based on data from over one million buy now, pay later applications, millennials (25-40) make up 47% of applicants and GenX (41-56) make up 28% of applicants [Equifax]

The average order paid by a BNPL loan is $149, compared to $141 with a credit card [NBC News]