How .99 Pricing Survives the Penny Shortage

The penny may be disappearing, but the psychology behind .99 pricing isn’t going anywhere.

You’re reading Monday Morning Economist, a free weekly newsletter that explores the economics behind pop culture and current events. Each issue reaches thousands of readers who want to understand the world a little differently. If you enjoy this post, you can support the newsletter by sharing it or by becoming a paid subscriber to help it grow:

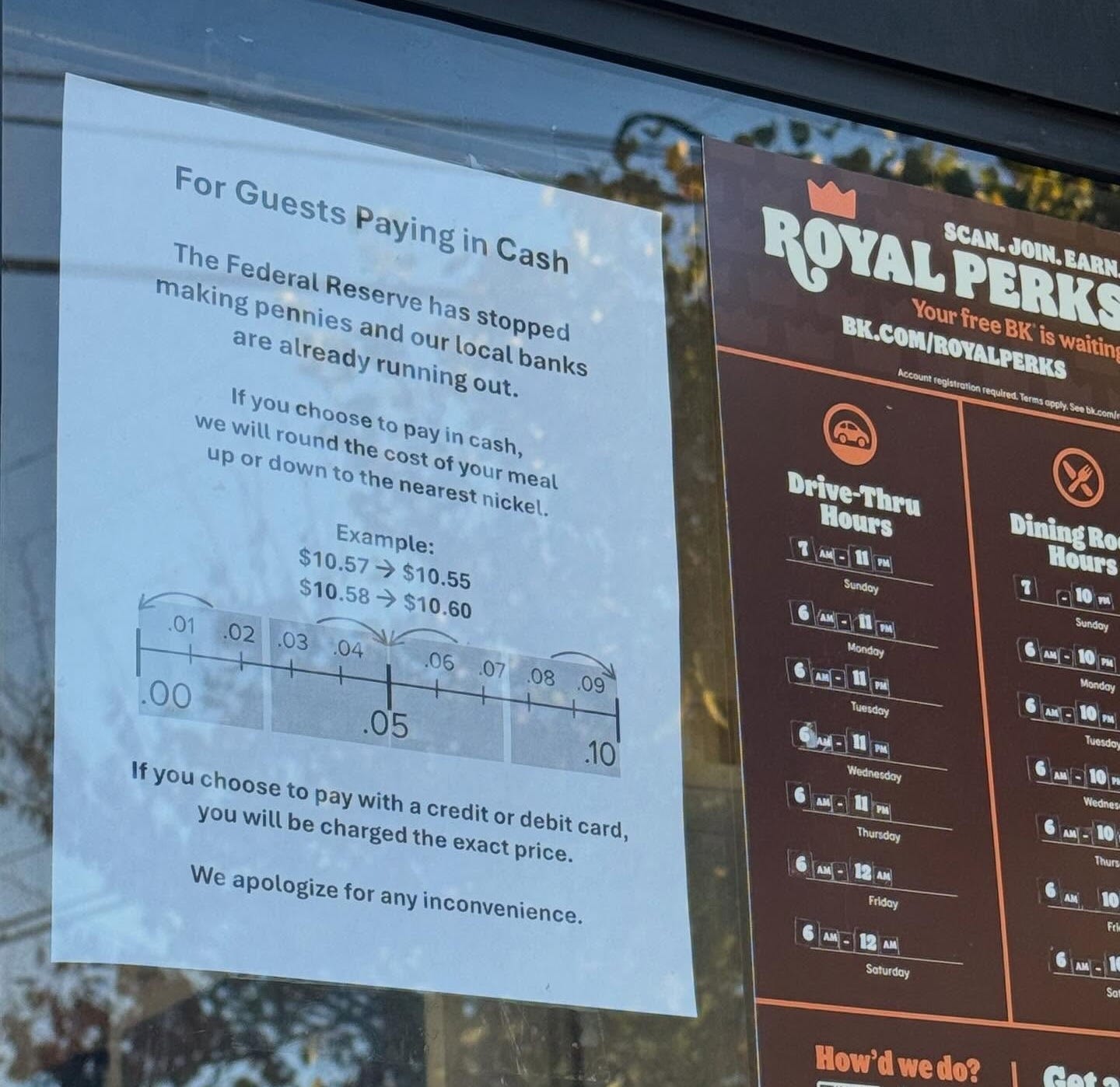

At a Burger King in Richmond, Virginia, a paper sign was taped on the drive-through window explaining that cash totals would be rounded to the nearest five cents because local banks were running out of pennies. It wasn’t fancy, but it got the point across.

Canada retired its penny back in 2013, and people eventually adjusted. Now that the U.S. has officially pressed its last penny, similar signs are popping up around the country. Some are taped to drive-thru windows, some printed on nice cardstock, some handwritten in Sharpie. All of them say a variant of the same message: “We’re out of pennies. Cash totals will be rounded.”

The rounding process is pretty easy to figure out, but unlike in Canada, the U.S. has not issued formal, national guidelines for rounding cash transactions. Typically, card customers pay the exact amount. Cash payments are rounded up or down to the nearest increment of five cents.

Some shoppers have complained about losing a cent or two, but most people have moved on to a different question entirely. It’s been popping up online and in comment sections everywhere: why don’t stores change their prices so rounding isn’t necessary?

And that’s where this story gets more interesting.

The Mystery of the Missing Pennies

Some stores have been quick to blame the Federal Reserve for the penny shortage, but that’s the wrong target. The Fed has never made coins; it only distributes whatever the U.S. Mint produces.

And earlier this year, the Trump administration instructed the Treasury to end penny production. The Mint carried out the order. So the Fed didn’t cut off supply to retailers; the supply simply stopped arriving.

But pennies weren’t circulating well long before the last one was minted. Americans have a habit of pulling them out of the economy. Back in the late 1990s, the Federal Reserve blamed a nationwide coin shortage on Americans “stockpiling pennies instead of circulating them through commercial transactions.” At the time, the Fed estimated there were more than 114 billion pennies in circulation. That’s about 426 per person, and yet stores still struggled to get enough.

We saw the same issue during the pandemic. As people used less cash, coins piled up in homes instead of moving through banks and retailers. Pennies may leave the Mint, but they rarely find their way back to banks.

So when the final penny rolled off the presses, the system was already strained once again. Signs went up, rounding started, and the penny quietly began to disappear. That part is pretty simple to explain. The next part is the head-scratcher for many Americans.

Why Not Just Change the Prices?

If pennies are getting harder to find, it seems logical for stores to solve the problem by pricing products so the final total ends in a five or a zero. Why not include the tax right in the sticker price and make the whole system cleaner before we ever get to the register? No pennies, no rounding, no confusion.

On paper, that idea works beautifully. But the United States makes it messy.

Other countries build sales taxes directly into the price tag, but the U.S. layers on taxes at the state, county, and even city level. A fast-food meal sold in Richmond, Virginia, can face a different tax rate than the same meal sold in a neighboring county thirty minutes away. Move that meal to Chicago, Phoenix, Seattle, or thousands of other municipalities, and the variation grows quickly.

That creates an advertising problem for national chains, which depend on national ads and consistent pricing. If Burger King runs a nationwide commercial for a $5.99 meal deal, customers will expect to see $5.99 on every menu board. If local stores adjusted the posted price to include the local taxes, customers might accuse the store of bait-and-switch when the price doesn’t exactly match the ad.

The result is a base price that stays the same nationwide, but a tax rate that gets applied at the register. It keeps advertising consistent without producing thousands of versions of the same promotion tailored to the ZIP code.

But it doesn’t explain why prices don’t simply shift to neat nickel amounts. Even if rounding were possible everywhere, most stores probably wouldn’t do it. And that’s because the real force shaping those numbers isn’t the tax code. It’s behavioral economics.

The Power of .99

Most retailers rely on a form of psychological pricing built on something behavioral economists call left-digit bias. We tend to focus on the leftmost digit much more than the rightmost one. A price of $9.99 feels meaningfully cheaper than $10.00, even though the difference is only a penny.

Retailers learned long ago that dropping a price by a single cent can move sales. The effect isn’t huge for every product, but it’s reliable enough that most stores keep doing it. You see it everywhere, from grocery aisles to online shopping carts. Shifting those prices to neat nickel increments would mean giving up a strategy that consistently shapes consumer behavior.

And left-digit bias isn’t limited to retail shelves. It’s a quiet force that influences entire markets. Gas stations cling to $3.499 because most people focus on the “3,” not the extra fraction of a cent. Used cars with 79,900 miles often sell faster (and for more) than identical cars with an odometer that just tipped over to 80,000.

Individually, these differences seem trivial. But they’re predictable, and businesses have leaned on them for decades. The numbers become signals, nudging us toward decisions we might not make if we focused on the full price.

Final Thoughts

The stakes are pretty small, but they’re not zero. Economists at the Richmond Fed analyzed thousands of cash transactions recorded in the Diary of Consumer Payment Choice. Over a three-day sample, most cash purchases ended in 0 or 5 cents and wouldn’t be affected by rounding at all. But among the remaining transactions, the pattern wasn’t random. Cash totals were more likely to end in 3, 4, 8, or 9 cents, amounts that would round up more often than they would round down. When the researchers scaled those patterns to the entire U.S. adult population, they estimated that rounding to the nearest nickel could cost consumers about $6 million a year.

Six million dollars across more than 330 million people is tiny in the grand scheme of things. But it’s also a reminder of how sensitive we are to even the smallest changes in prices, especially when they show up at the register instead of the shelf.

And that’s the irony at the center of this whole story. The penny is disappearing, but the pricing habits built around it aren’t. Even without the coin itself, the psychology it shaped still lives on in the price endings we see every day.

In a country that’s officially a penny short, the power of .99 is still doing just fine.

If you enjoyed this story, consider sharing it with someone who might appreciate a look at the economics hiding in plain sight. A friend, a coworker, or that person who always has opinions about prices. All are fair game.

The first pennies were struck in 1793 of pure copper (a cheap metal at the time) and featured a woman with flowing hair symbolizing liberty [Forbes]

There are no official rounding rules in the United States, but H.R.3761 was a bill introduced in 1980 that would allow rounding [101st U.S. Congress]

About 70 percent of cash payments were for $10 or less [Federal Reserve Bank of Atlanta]

Retail sales taxes are an essential part of most states’ revenue toolkits, responsible for 32% of state tax collections and 13% of local tax collections [Tax Foundation]

The Coinage Act of 1792 established a national mint located in Philadelphia [U.S. Mint]

My theory is if a singular coin can't be used to purchase anything, it should be eliminated. Is there a single thing that can be purchased for a penny, nickel or dime? Get rid of them all. Round prices to the nearest quarter. Or at least just round to the dime, so we can get rid of the hundredth digit in pricing.

"In a country that’s officially a penny short", pure poetry

I wonder if the left-digit bias effect is greater when it also bumps the price up to the next order of magnitude, i.e., $9.99 to $10.00 vs $2.99 to $3.00. I also wonder if people who work with numbers all day have the same propensity for it as the general populace, or if it's been trained out of them to some degree.

Lots of finger pointing as to which part of our monetary system is "to blame" for the penny going away, but few seem to be blaming the devaluation of our currency via rampant, unchecked inflation. Hmmm